Search our website enhanced by Google.

Tuesday, 7 May 2024

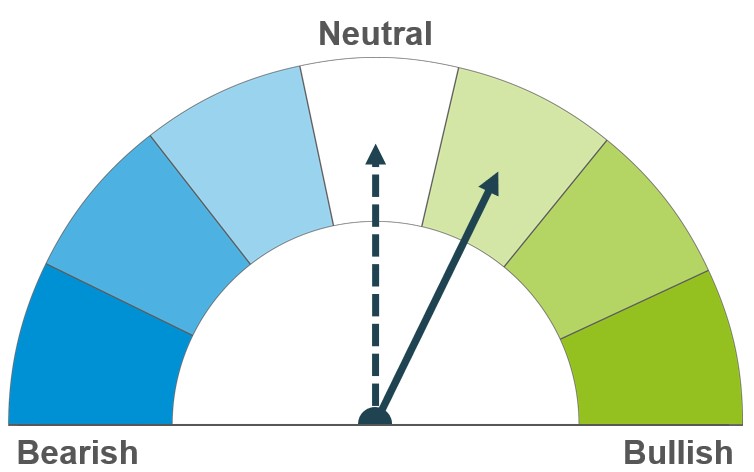

Unfavourable weather forecasts for wheat crops in Russia and other major exporting countries continue to drive prices. Re-positioning ahead of Friday’s USDA report is likely to influence markets this week too.

Flooding in Brazil and less than ideal weather for planting in the US mean uncertainty over the outlook for global maize supplies. Any issues with wheat could push further feed demand to maize.

While larger barley crops are currently expected for key producers in 2024/25, it’s still early. The uncertain outlook for wheat is a key influence on barley currently.

Ongoing worries about the impact of dry weather on wheat crops in Russia pushed markets higher last week.

Prices dipped early last week after rain was forecast and speculative traders booked profits. However, the rises resumed later in the week after limited rain fell and Russian forecaster IKAR trimmed its crop forecast from 93.0 Mt to 91.0 Mt. This is now slightly below 2023’s crop of 91.6 Mt (Reuters). Buying by speculative traders and maize crop concerns also contributed.

Yesterday, Dec-24 wheat futures reached their highest levels since August 2023; Chicago wheat futures rose $9.09/t to $254.70/t, while Paris wheat futures gained €9.50/t to €250.50/t. Dec-24 Chicago maize futures also reached its highest price since 11 January at $192.32/t.

Following adverse weather and damage from leafhoppers, the Buenos Aries Grain Exchange cut its estimate of the Argentinian maize crop by 3.0 Mt to 46.5 Mt. Meanwhile, heavy rain and hot, dry conditions are causing concern for maize in different parts of Brazil. Slower planting in the US due to rain is also adding to nerves for maize. After the market closed yesterday, the USDA reported that 36% of the US maize crop was planted by 5 May, behind the 39% the market had expected (LSEG).

US winter wheat crop conditions were slightly improved between 28 April and 5 May, while spring wheat planting continues at pace.

French crop condition scores were stable for soft wheat and barley, with a slight improvement for spring barley (FranceAgriMer). Meanwhile, German bread wheat and malting barley prices were supported by the uncertain impact of recent frosts (AMI).

With more uncertainty over the outlook for markets, this is a key time to watch markets. The USDA releases its first projections of global supply and demand in 2024/25 on Friday (10 May).

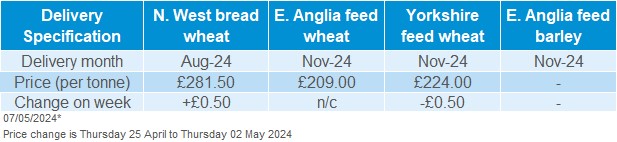

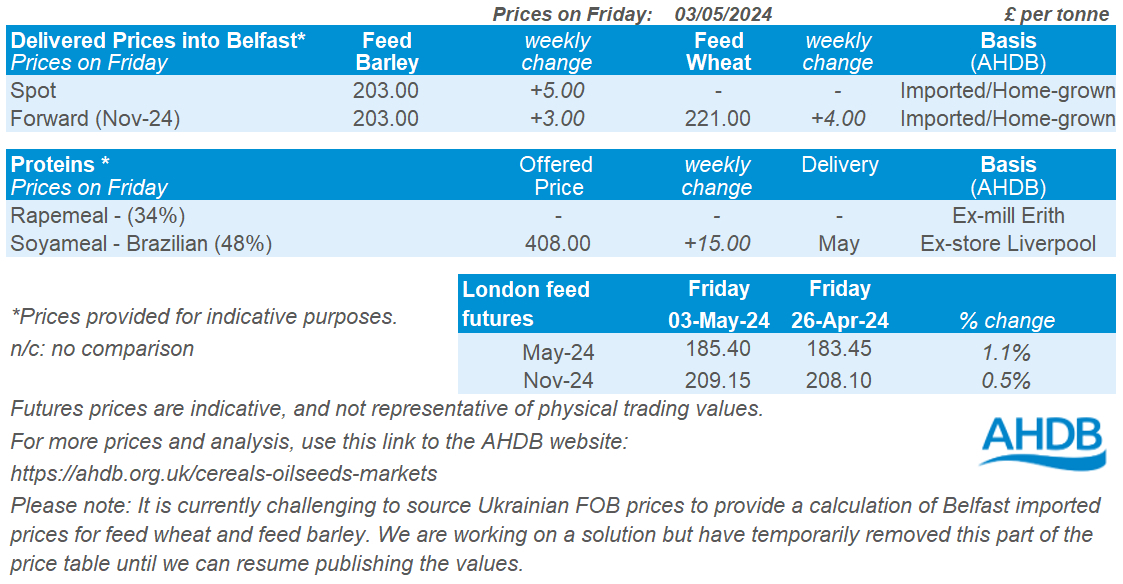

New crop (Nov-24) UK feed wheat futures gained £1.05/t last week (Friday-Friday) to settle at £209.15/t. Meanwhile. The May-24 contract gained £1.95/t over the same period to £185.40/t.

Bread wheat to be delivered in the North West at harvest was reported at £281.50/t last week, up £0.50/t Thursday – Thursday.

AHDB’s latest crop report showed GB winter cereal crop condition scores at the end of April were higher than late-March but still sharply lower than in recent years. For example, 45% of winter wheat is now rated as in a good or excellent condition, up from 34% in late-March but well below the 88% a year earlier. Field work for winter crops is also still behind and there is a wide range in development stages.

Although many growers have now been able to drill spring crops, there are still empty fields and there are only a few days left to plant spring barley in most of the UK.

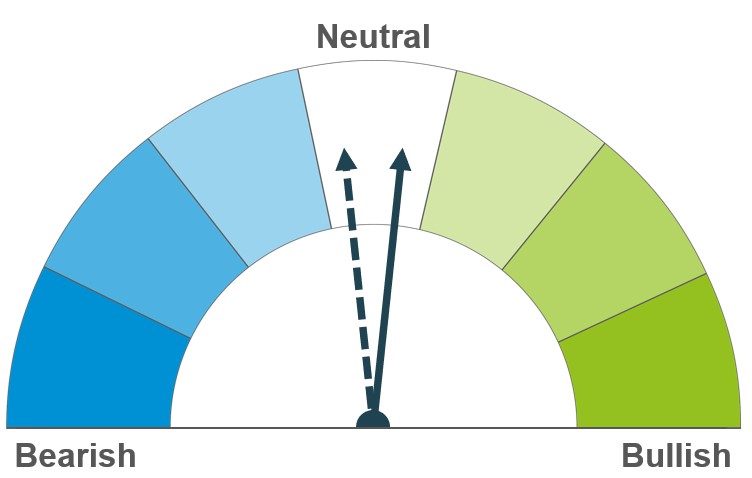

Tighter global rapeseed supplies are forecast in 2024/25. However, the wider oilseed market currently looks well supplied and total demand is relatively weak, influencing the overall sentiment.

Despite some concerns over Brazilian harvest progress, global soyabean supplies continue to look ample longer-term.

Despite some weakness in vegetable oil markets, old crop (May-24) and new crop (Nov-24) Chicago soyabean futures gained 6.5% and 3.8% respectively from 26 April to 06 May. The key driver of this support was adverse weather in Brazil, fuelling concerns over crop losses.

Floods have disrupted soyabean harvest progress in top exporter Brazil. Crops in the Rio Grande do Sul region have been hit with heavy rains in the final stages of harvest. In the south of this region, it’s estimated that 40% of the soyabean crop remains to be harvested (LSEG). More rain is due in the area over the coming week, something to watch out for.

Despite concerns over abnormal levels of rain across the US plains as of late, US soyabean plantings are ahead of average for this point in the season. In the USDA’s weekly crop progress report released yesterday, US soyabean plantings were 25% complete as of 05 May. This is compared to 18% complete the week prior, and the five-year average of 21% complete for this point in the season.

Support in Chicago soyabean futures was capped last week due to sliding soya oil prices. Weak demand in the wider vegetable oil complex, as well as pressure in crude oil markets, means Chicago soyabean oil futures (May-24) were pressured 3.9% on the week (26 April to 06 May). Nearby Brent crude oil futures were pressured 6.9% over the same period.

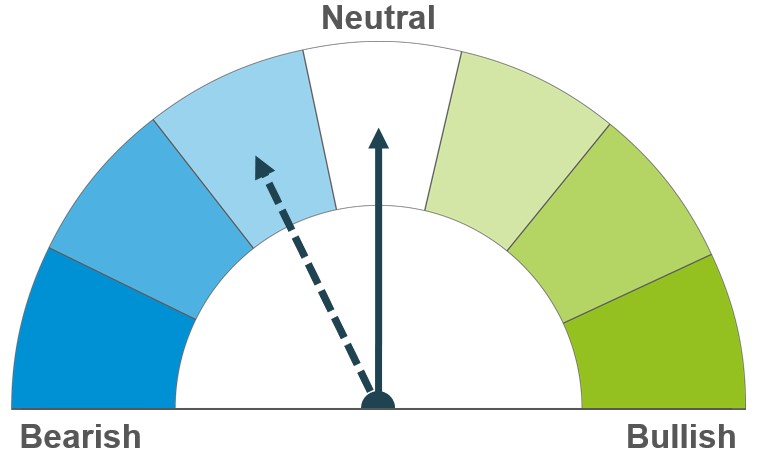

Paris rapeseed futures followed upwards movement in soyabean markets. The Nov-24 contract gained €21.50/t last week (26 April to 06 May), ending yesterday’s session at €488.50/t.

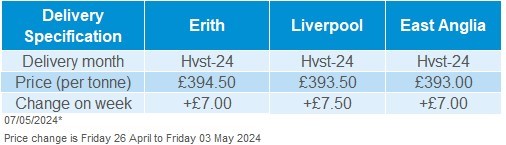

Domestic rapeseed prices followed futures market movements last week (Friday to Friday). Rapeseed delivered into Erith for May delivery was quoted at £387.50/t on Friday, up £8.00/t on the week. Delivery into Erith for November was also up £8.00/t, quoted at £405.50/t.

In AHDB’s latest crop condition and development report, only 47% of the winter oilseed rape crop was rated as in good or excellent condition. This represents an improvement from late March (31%) but is still well below the 66% with the same rating at the end of April 2023.

Last Monday, Stratégie Grains released its latest EU oilseeds reports including an estimate for the 2024/25 rapeseed crop. The EU rapeseed crop is now pegged at 18.1 Mt, relatively unchanged on the previous month’s estimate. This is down 9.0% on the year.

Statistics Canada is due to release estimates of Canadian crop stocks as at the end of March today. In a Reuters pre-report poll, analysts on average expect canola stocks to reach 8.3 Mt, this would be up from the March estimate of 7.0 Mt.

While AHDB seeks to ensure that the information contained on this webpage is accurate at the time of publication, no warranty is given in respect of the information and data provided. You are responsible for how you use the information. To the maximum extent permitted by law, AHDB accepts no liability for loss, damage or injury howsoever caused or suffered (including that caused by negligence) directly or indirectly in relation to the information or data provided in this publication.

All intellectual property rights in the information and data on this webpage belong to or are licensed by AHDB. You are authorised to use such information for your internal business purposes only and you must not provide this information to any other third parties, including further publication of the information, or for commercial gain in any way whatsoever without the prior written permission of AHDB for each third party disclosure, publication or commercial arrangement. For more information, please see our Terms of Use and Privacy Notice or contact the Director of Corporate Affairs at info@ahdb.org.uk © Agriculture and Horticulture Development Board. All rights reserved.