Search our website enhanced by Google.

Thursday, 11 August 2022

The chosen network for cheese consists of the UK, New Zealand, EU, USA and China. The EU is the world’s largest cheese exporter and is a key trading partner for the UK. While the UK produces more cheese than New Zealand, domestic consumption of cheese in New Zealand is much lower in comparison and so the country has a considerable exportable surplus. China is a key market for New Zealand cheese.

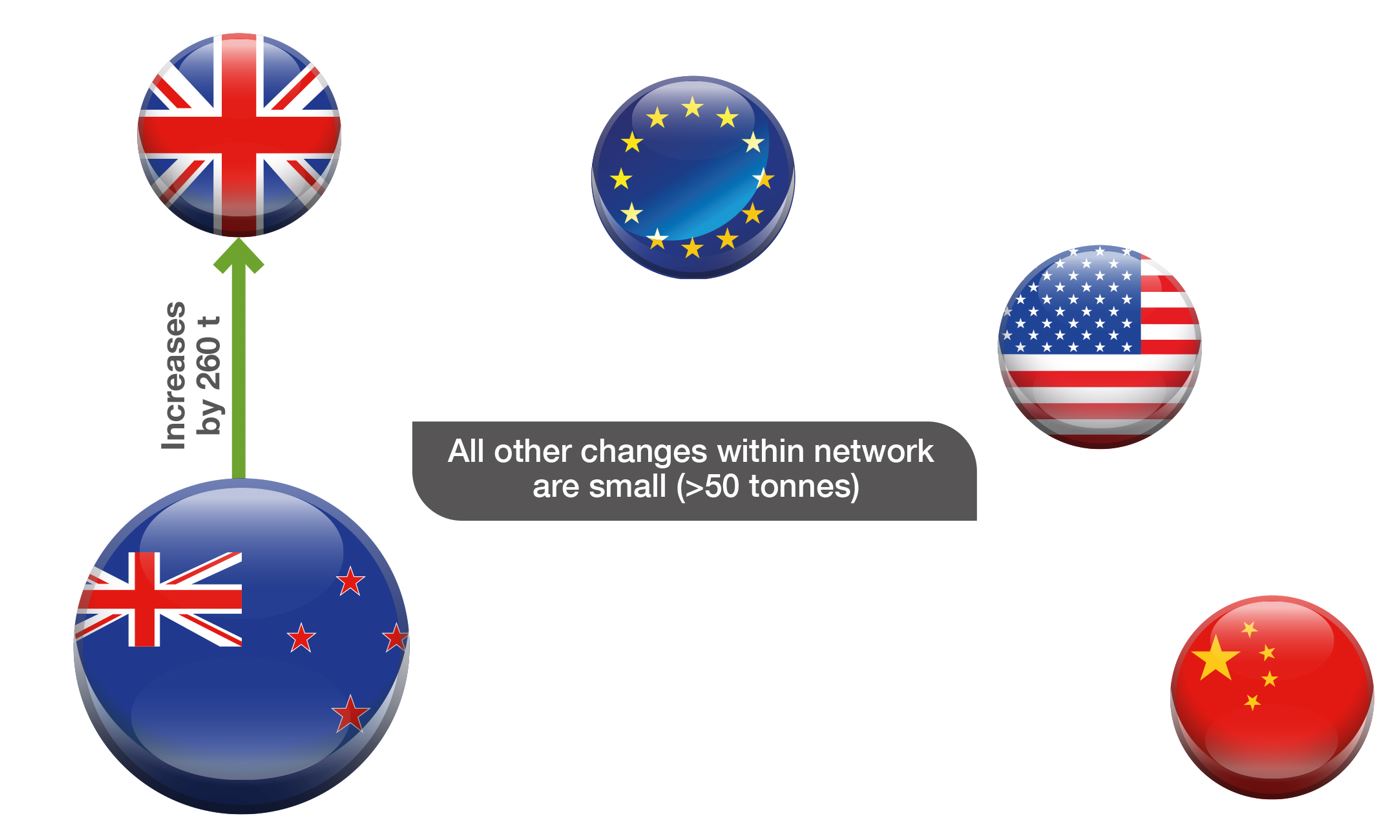

The model predicts that UK cheese imports from New Zealand will increase by 260 tonnes (194%) as shown in Figure 1. Total UK cheese imports will increase by 190 tonnes (less than 0.1%). The higher number of cheese imports from New Zealand will partially displace cheese imports from the USA and EU.

In order to send more cheese to the UK, New Zealand’s cheese production will increase by around 190 tonnes (0.1%) and less cheese would be sent to other countries in the network.

Figure 1. Network showing main changes in cheese trade flows

Source: AHDB/Harper Adams University

The predicted impact of the UK-New Zealand trade deal on UK prices is small (<0.1%) with an even smaller drop in production in percentage terms. The New Zealand farming sector is predicted to see a slight increase in production (0.1%) and prices, with the price paid to farmers only 0.01% higher.

The network for butter is the same as for cheese. New Zealand exports more than 80% of the butter it produces. China is a key export market for New Zealand butter, while for the UK, the main market is the EU. The USA is also an important market for EU and New Zealand butter.

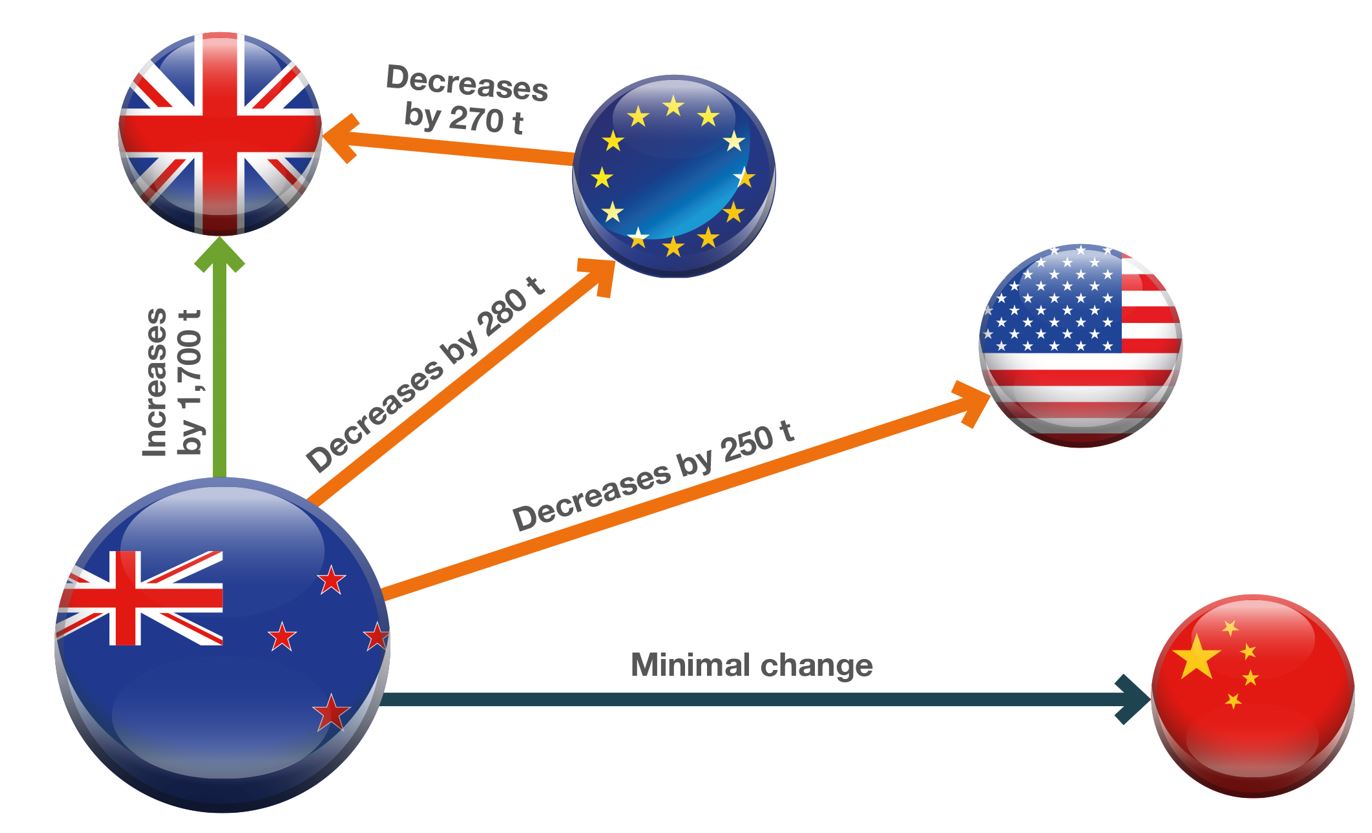

According to the model, the UK-New Zealand trade deal will lead to New Zealand butter exports to the UK increasing by 1,700 tonnes (209%) as shown in Figure 2. Total UK butter imports increase by 2% (1,500 tonnes), mainly due to the additional volume coming in from New Zealand, although some of this is offset by a drop in imports from the EU and USA.

Figure 2. Network showing main changes in butter trade flows

Source: AHDB/Harper Adams University

The model calculates that UK butter production will fall by 80 tonnes (less than 0.1%), while New Zealand butter output will increase by 1,100 tonnes (0.8%). In terms of prices, the UK retail price for butter would drop by less than 0.5% and there is negligible change in the price paid to farmers. New Zealand farmers would be paid less than 1% more than the 2018-20 baseline.